The Economy Grows, Inflation Heads Up, Culture Wars Heat Up

It should come as no surprise that the abrupt end of the post-World War II geopolitical settlement calls for a reappraisal of the future of the American economy. Nor should it be a surprise that such a reappraisal is made doubly difficult when accompanied by sanctions that are disrupting markets from oil to wheat to battery components, and a Federal Reserve Board seeking to reconnect with the reality facing consumers.

Economic History Does Not Always Repeat Itself

Begin by rejecting the idea that we can divine where the economy is headed by studying the economy’s reaction to the Arab oil embargos of 1973 and 1978-9. Then, oil prices increased cumulatively ten-fold, this time they have at most doubled from a low point at the end of last year, to their high point this month. Then, inflation was running at annual rate of 14.8 per cent, this time, at 7.8 percent, it is at about half that rate. Then, the Fed raised its benchmark interest rate to over 20 per cent. This time, even if the central bank were to increase rates by one-half of one per cent rather than one-quarter, and repeat the process 11 times as contemplated, rates would be in the not-unusual 5-6 per cent range, one-third of the level during the last round of inflation-fighting. Perhaps more is needed, but at least the Fed is tackling a problem that its European counterpart, faced with an inflation rate of almost 6 per cent and rising, refuses to confront. Unfortunately for the President’s Democrats, Powell has probably entered the anti-inflation lists too late to tamp down inflation by the November mid-terms.

None of this is intended to minimize the economic and social consequences of the current round of inflation. It is merely to suggest that our economic past is unlikely to prove prologue.

Growth Slows But Doesn’t Stop

Start with the fact that the American economy is growing and is expected by Goldman Sachs’ forecasters to continue to grow at an above-trend 3.6 percent next year. Factories seem to be springing up everywhere in response to supply-chain interruptions affecting overseas orders, and to hoped-for benefits from President Biden’s protectionism or, if you prefer, deglobalization. Airlines are fully booked for the next several months with travel-eager customers sitting on large piles of excess savings and “collecting experiences” of which they have been deprived during two years of lockdowns – visits to Disneyland are high on the list. Over 11 million job openings remain unfilled, the economy added 678,000 jobs last month, the unemployment rate is a relatively low 3.8 percent, and initial claims for unemployment insurance are at their lowest level in over 50 years.

Take a further step into the land of euphoria and explain away some negative indicators. Vehicle sales are down. But dealer-reported price increases of 35 percent for new and used cars suggest that a shortage of components such as chips, rather than lack of demand, is to blame. Sales of new houses have declined, but builders attribute that to their inability to obtain enough key materials or hire enough workers to meet demand. As with vehicles, prices remain high. Whether that optimistic version of the reason for the sales drop or elevated prices will survive the new era of 4.5-5 percent mortgage rates, the highest since January 2019, remains to be seen.

None of this is intended as an application for admission to the Pangloss School of Economic Studies. So be warned that inflation is scary, and it is easy to underestimate how consumers and investors will react when the latest inflation figure clocks in at double digits, as it likely will, with the largest increases in states that are considered electoral battlegrounds, won by tiny margins in 2020.

Perceptions Can Trump Data

Then, too, there are times when citizens’ perceptions are more reliable than economists’ data-driven predictions. Now might be one such time. Those perception are largely negative, as reflected in two bits of data. Consumer confidence fell in February for the second consecutive month. And 57.8 percent of Americans disapprove of the President’s management of the economy while only 37.7 percent approve. Many cite what they consider wild spending that have caused many to prefer relief payments to paychecks, proving that necessity is the mother of work.

In addition, neither man nor woman lives by bread alone, and an economist with a crystal ball that does not allow for that fact can be a menace. The late, great F.A. Hayek wrote, “Nobody can be a great economist who is only an economist – and … the economist who is only an economist is likely to become a nuisance if not a positive danger.” He would not have considered irrelevant the rancorous culture war now underway.

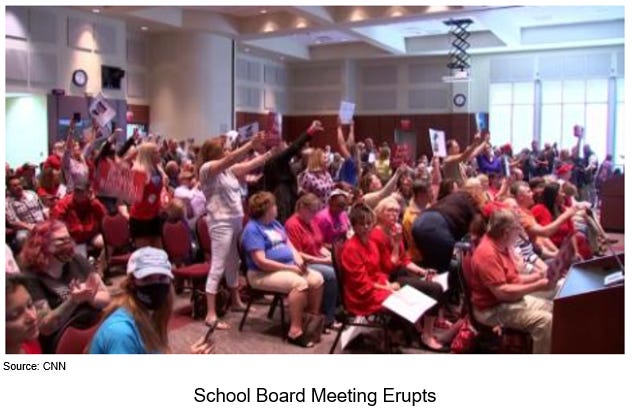

Culture War Matters But May Elude Pollsters

That culture war is the great unmeasurable of American politics. School board meetings, once ill-attended and boring, have become shouting matches between parents who are “woke” and want kids taught about white privilege, and those who prefer emphasis on the Three Rs. Once- routine elections of local law enforcement officials, have become battles between candidates who see their job as emptying the prisons, and tough-on-crime advocates. It is neighbor vs. neighbor when it comes to jab mandates, gun control and other issues. It is generally agreed that voters on the conservative side of these controversies are the ones most likely to refuse to respond to pollsters.

These me-and-my-kids-are-at-stake elections generate more heat than those to decide which of two strangers should get a congressional seat. These are not battles over far away issues about which voters know or care very little. They are down home and personal. And these battles might be a more powerful determinant of who next occupies the Oval Office than the latest measurement of the nation’s GDP.