Jobs and More Jobs. Debt and More Debt.

The economy is doing better than most people had hoped. The failure of the warring politicians to extend benefits has not completely derailed it. A vaccine seems to be on the horizon, ready for use before year end. All that good news is adding to mounting pessimism about the future of the American economy and the nation.

Start with the economy.

Total employment increased in August by 1.4 million, and average hourly earnings and the average work week rose. The unemployment rate dropped for the fourth consecutive month, from 10.2% in July to 8.4%, and the number of unemployed fell by 2.8 million. The labor force participation rate rose. Despite some negatives - 13.6 million workers remain jobless - overall, an upbeat report.

Economic activity in the manufacturing sector increased. The ISM index rose to 56 in August, with anything over 50 indicating growth.

New orders for durable goods (products designed to last at least three years) rose 11.2% in July, to the highest level since December 2006.

Sales of new single-family homes rose 13.9% in July from June, and 36.3% over year-earlier levels to their highest level in 14 years. Construction of those homes rose in July at the fastest rate since February, before the pandemic hit.

And the Federal Reserve survey of business conditions around the country, released last week, finds that "Economic activity increased among most districts ... manufacturing rose ... consumer spending continued to pick up ... residential construction was a bright spot ... employment increased overall ... firms continued to experience difficulty finding necessary labor...". Good news, especially for Trump, who believes the direction in which the economy is moving is more important to his chances than its currently depressed absolute level.

Add to the relatively good economic news even better news about the development of vaccines. The Centers for Disease Control has notified 50 states and major cities to be prepared to distribute a vaccine to health care workers and vulnerable groups as soon as next month or early November. The speed with which multiple vaccines have been developed and distributed in anticipation of proof of their safety and effectiveness is due in good part to Trump's decision to throw government money at the problem and to use his trusty scissors to cut red tape and regulatory delay. That should permit him to change the narrative developed by the Democrats - he fumbled the reaction to the outbreak - to one touting his leadership in early development of vaccines.

The good economic and medical news has had an oddly perverse effect on many Americans. The threat of protracted recession and continued outbreaks are the devils we know. The nature of the economy that will emerge in what is likely to be the near future is a known unknown. Unlike Ethel Merman in the musical Gypsy, Americans doubt that everything's coming up roses and daffodils and sunshine and lollipops.

Some two-thirds of Americans believe the country is on the wrong track. Consumer confidence declined in both July and August. The nation's CEOs, who determine investment and hiring decisions, "remain pessimistic" according to the non-profit Conference Board. Pew Research Center pollsters find that "Americans continue to give their country negative ratings for living up to several key democratic ideals and principles." Few (30%) believe the government is open and transparent, and even fewer (27%) believe elected officials face serious consequences for misconduct.

One worry is that treasury secretary Steve Mnuchin and officials such as Federal Reserve governor Lael Brainard and Federal Reserve Bank of Chicago president Charles Evans are right that the economy needs another round of stimulus, even though the Lindsey Group reckons that the loss of $600 weekly insurance top-up payments "is survivable" because locked-in consumers have accumulated $1.05 trillion of excess savings, which "can compensate for the lost unemployment benefits for over 16 months." Good thing: there is little prospect that Democrats, eager to keep the economy on pause until after the election, will sign on to any deal acceptable to the Republicans.

Add the unsettling effects of protests that all-too-often are accompanied by fiery riots and looting. Even anti-Trump commentators say Biden's milksop reaction was too little, too late to reassure law-and-order voters, especially suburban women who have drifted away from Trump in response to his unpleasant personal behavior. They would be forgiven for wondering whether that nice Mr. Biden will have the will and energy to protect them from a reprise of "burn, baby, burn", the 1965 slogan adopted by rioters in Los Angeles. The Washington Post reports that "spikes in favor of the Black Lives Matter movement have "subsided", especially among white Americans, or as that "woke" newspaper would have it, "White Americans". A poll in Wisconsin, later to be the scene of the Kenosha riots and the torching of small businesses, found that 61%-38% support for BLM in mid-June evened to 48%-48% last month.

Meanwhile, fears mount that Trump and Biden are contesting for control of a seriously scarred nation. The winner will inherit a nation more bitterly divided than ever as both sides take to the courts to contest the results and accuse each other of vote-counting skulduggery. Trump has attacked the use of mail-in ballots, Hillary Clinton is urging Biden not to concede "under any circumstances because I think this is going to drag out, and eventually we will win if we don't give an inch...". George W. Bush was declared the winner over Al Gore on December 12, 2000, so we will more than likely be toasting the President of the United States on Thanksgiving Day, whomever he may be, and wishing him a happy New Year, whomever he may be.

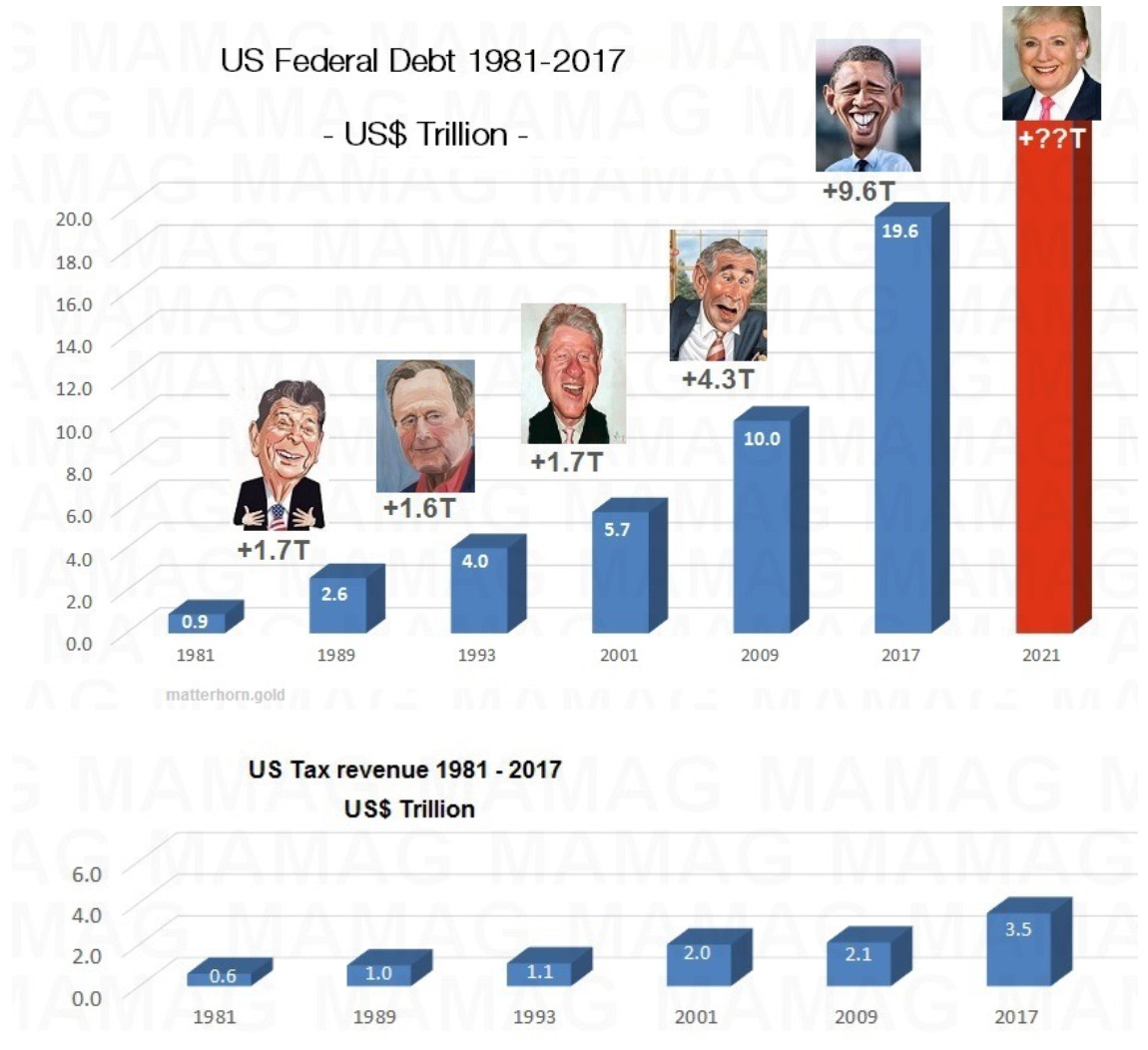

Having promised to cut taxes (Trump), or increase spending (Biden), the winner will inherit a nation with extraordinary deficits (17.9% of GDP this fiscal year reckons the Brookings Institution), more deeply in debt relative to the size of the economy than at any time since 1946. It will have joined Greece and Italy as countries with accumulated IOUs in excess of their GDP. He will inherit an economy with its small business sector decimated, in which much capital, such as office space, has become obsolete and with many workers struggling to adapt to a world in which work-at-home and e-commerce demand skills they do not possess - an under-skilled group that might easily become a new under-class. He will inherit a consumer class that might be shell-shocked into miserliness.

Those are problems that, in the words of Tevye, the poor milkman in "Fiddler on the Roof", are so complex "They would cross a rabbi's eyes." Neither candidate can reasonably be said to have the wisdom of a wise cleric. Cometh the time, cometh not the man.